Original Link: https://www.anandtech.com/show/18845/amd-reports-q1-2023-earnings-back-into-the-red-as-client-sales-crumble

AMD Reports Q1 2023 Earnings: Slipping Back into the Red as Client Sales Crumble

by Ryan Smith on May 3, 2023 7:00 AM EST- Posted in

- CPUs

- AMD

- GPUs

- Financial Results

Continuing our earnings season coverage for Q1’2023, today we have the yin to Intel’s yang, AMD. The number-two x86 chip and discrete GPU maker has been enjoying a growing diet of Intel’s lunch for much of the past two years, but like the rest of the tech industry, AMD is now seeing a significant drop-off in sales as businesses and consumers alike curtail tech spending. So, like numerous other companies in this field, AMD has been bracing themselves for a rough first half of the year, after managing to beat the pack in Q4’2022 by posting a small profit.

For the first quarter of 2023, AMD reported $5.4B in revenue, continuing the year-over-year slide they’ve been experiencing throughout the past few quarters. All told, AMD’s top-line revenue dropped by 9% versus Q1’22, which is a much smaller drop than some of its rivals, but it’s a situation that has also been artificially buoyed by the Xilinx acquisition. That acquisition, which closed late into Q1’22, has boosted AMD’s revenue significantly on a year-over-year basis for the past few quarters – suffice it to say, it was not a small acquisition – though that is coming to an end now that AMD has owned Xilinx for over a full year.

The additional revenue and sales that Xilinx has brought to the table has shifted AMD in some important ways, but it hasn’t helped to halt the fundamental drop in sales that the tech industry is facing. As a result, the hit to AMD’s income has been significant; operating incomes dropped by 115% to negative $145M, and net income saw a similar dive into the red with a 118% drop, for a final tally of a $139M loss.

| AMD Q1 2023 Financial Results (GAAP) | ||||||

| Q1'2023 | Q1'2022 | Q4'2022 | Y/Y | |||

| Revenue | $5.4B | $5.9B | $5.6B | -9% | ||

| Gross Margin | 44% | 48% | 43% | -4.0pp | ||

| Operating Income | -$145M | $951B | -$149M | -115% | ||

| Net Income | -$139M | $786M | $21M | -118% | ||

| Earnings Per Share | -$0.09 | $0.46 | $0.01 | -116% | ||

Though far from rival Intel’s record-breaking loss, the most recent quarter is still a black eye for the black team, who previously had been enjoying a run-up in business over the past several years on the back of the Zen renaissance. The one silver lining, at least, is that AMD’s core businesses as a whole have remained profitable on a non-GAAP basis; AMD’s GAAP loss was driven largely by structural costs, particularly $305M in stock-based compensation, and $823M written down via amortization of acquired (Xilinx) intangible assets. All of which has been a very common refrain for a lot of tech companies over the past couple of quarters. AMD is sitting on a further $23B of intangible Xilinx assets – largely covering the patents and other technologies AMD received in the acquisition and are now slowly losing value – so these sorts of write-down will be continuing for some time.

| AMD Q1 2023 Reporting Segments | |||||

| Q1'2023 | Q1'2022 | Q4'2022 | |||

|

Data Center

|

|||||

| Revenue | $1295M | $1293M | $1665M | ||

| Operating Income | $148M | $427M | $444M | ||

|

Client

|

|||||

| Revenue | $739M | $2124M | $903M | ||

| Operating Income | -$172M | $692M | -$152M | ||

|

Gaming

|

|||||

| Revenue | $1757M | $1875M | $1644M | ||

| Operating Income | $314M | $358M | $266M | ||

|

Embedded

|

|||||

| Revenue | $1562M | $595M | $1397M | ||

| Operating Income | $798M | $277M | $699M | ||

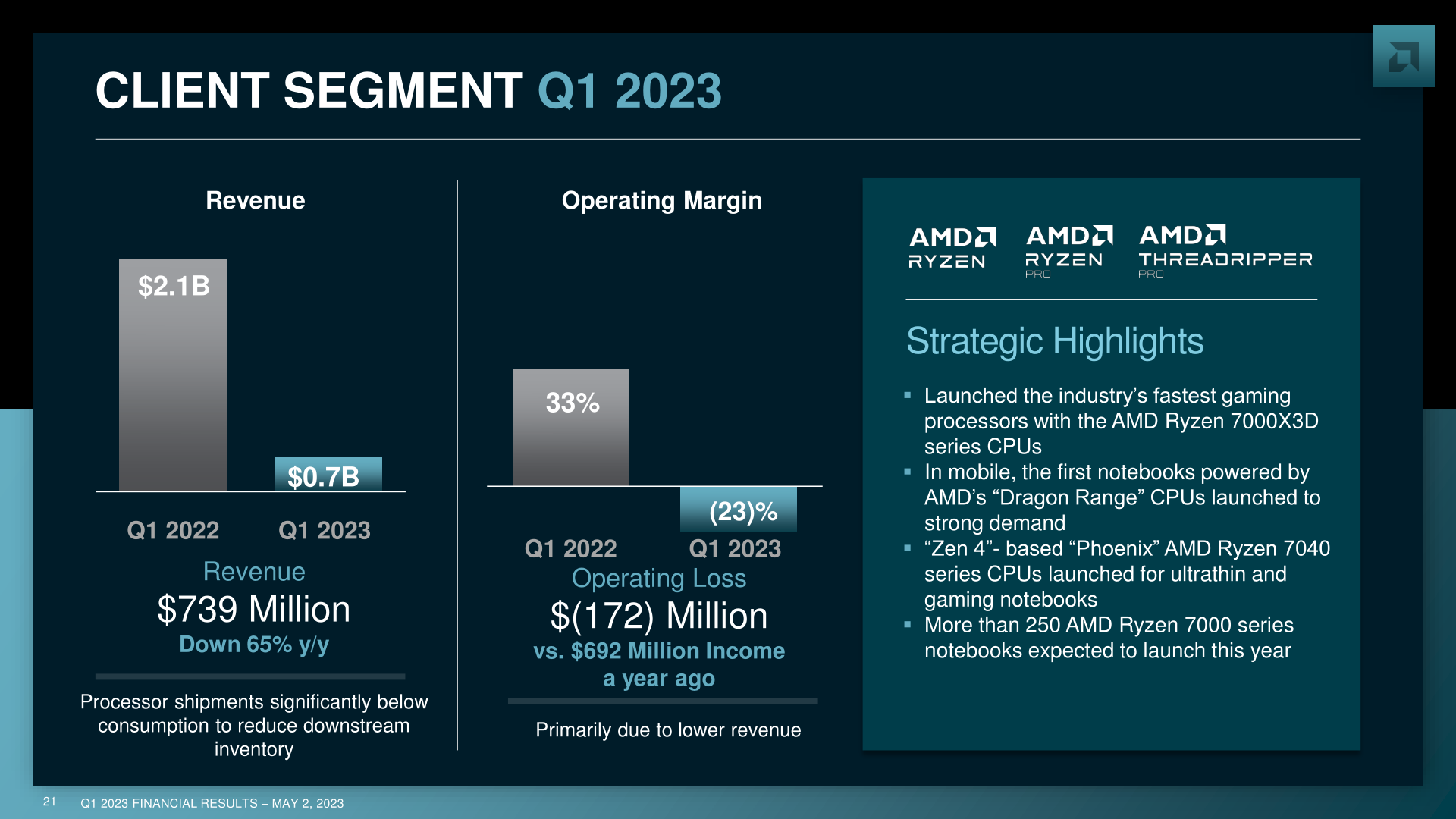

Moving on to the performance of AMD’s individual segments, we start with AMD’s client segment, which encompasses their desktop and notebook CPU sales, as well as chipsets. The utter collapse of client demand that started in the second half of the year has accelerated further in Q1’23, resulting in AMD’s client revenue dropping by a staggering 65%.

Altogether, AMD booked just $739M in client revenue for the quarter, their lowest in years. Client sales have been the biggest drop across the entire tech industry, and AMD has fared much worse than other tech companies in this regard, as evidenced by a 65% revenue drop when industry-wide client shipments are down by closer to 30-40%. This has also driven the operating income for this segment significantly into the red, with AMD taking a $172M loss on the division.

As with rival Intel, the drop in client sales is being compounded by AMD’s OEM customers working to reduce their own inventories, meaning that they’re ordering fewer chips to replace what they do sell. So AMD has far fewer opportunities to sell chips so long as that customer inventory bubble remains. Client ASPs are also down YoY, though AMD isn’t specifying by how much. The one bit of good news here is that AMD believes that they’ve finally hit the bottom of the client sales collapse in Q1. If AMD is right, it will still take until the second half of the year before they recover, but it means the company is going to be able to put the worst behind them and things only get better from here.

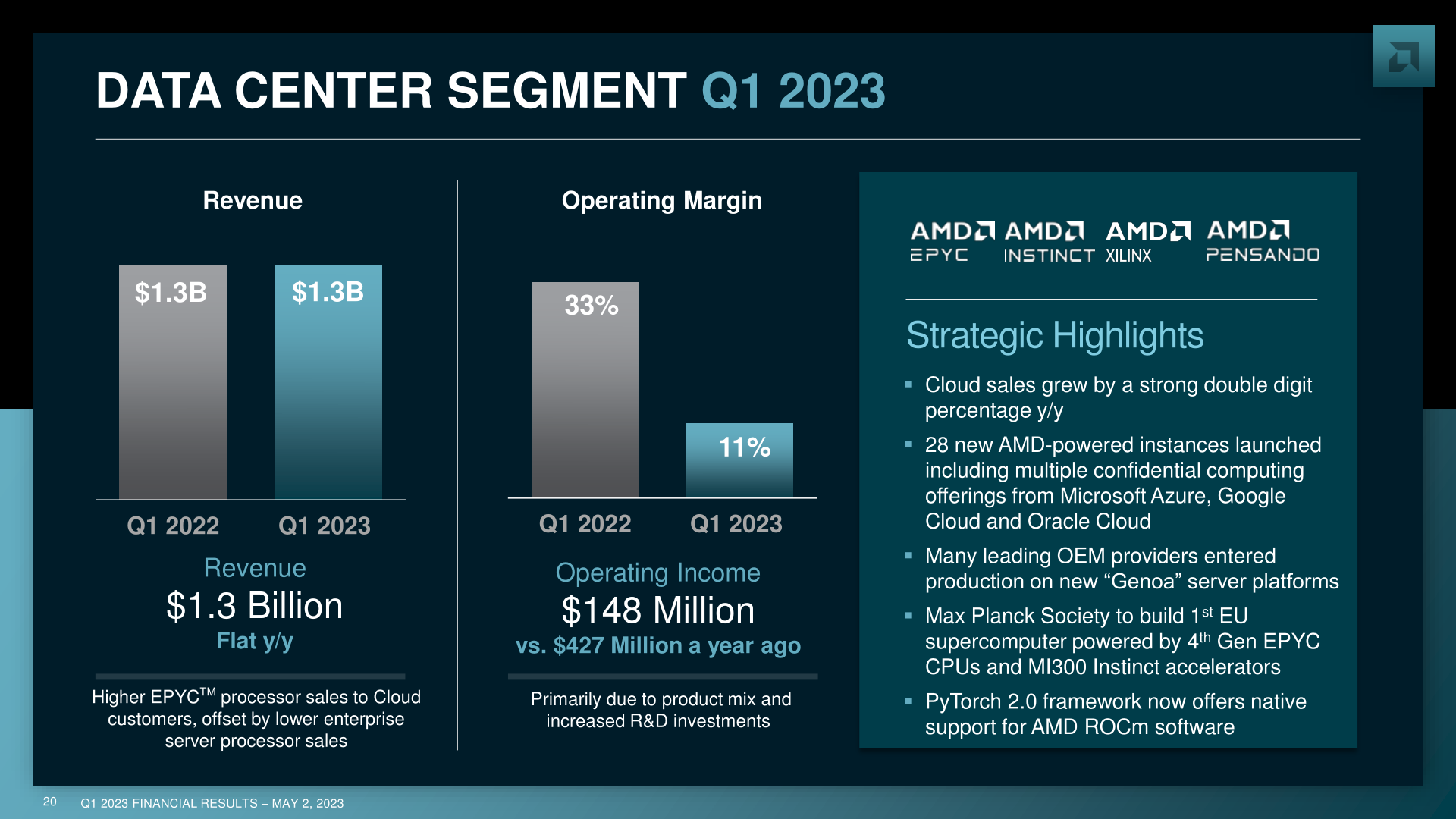

Meanwhile AMD’s Data Center segment has also seen its own challenges in recent quarters as data center customers slow their spending as well, though AMD has fared relatively better here though a combination of the Xilinx acquisition and successfully growing the company’s overall data center market share. As a result, AMD’s data center revenue was flat on a year-over-year basis at $1.3 billion.

The operating income for the segment did take a hit, however, dropping by 65% to $148M, a margin of just 11%. The relatively high margins on data center products to begin with has allowed AMD to stay in the black on this segment, albeit thinly. Propping up the segment for Q1 has been higher EPYC CPU sales to cloud customers, counteracting a drop in sales with enterprise customers. AMD’s new EPYC 9004 Genoa processors were also shipping in this quarter, though it doesn’t sound like they had a huge impact on AMD’s bottom line quite yet, as customers are still ramping up server production. It’s also worth noting that, following the Xilinx acquisition, AMD books part of their FPGA revenues here – basically, any product aimed at data center customers falls under this segment – so it’s likely AMD is also enjoying some year-over-year revenue stability thanks to those sales.

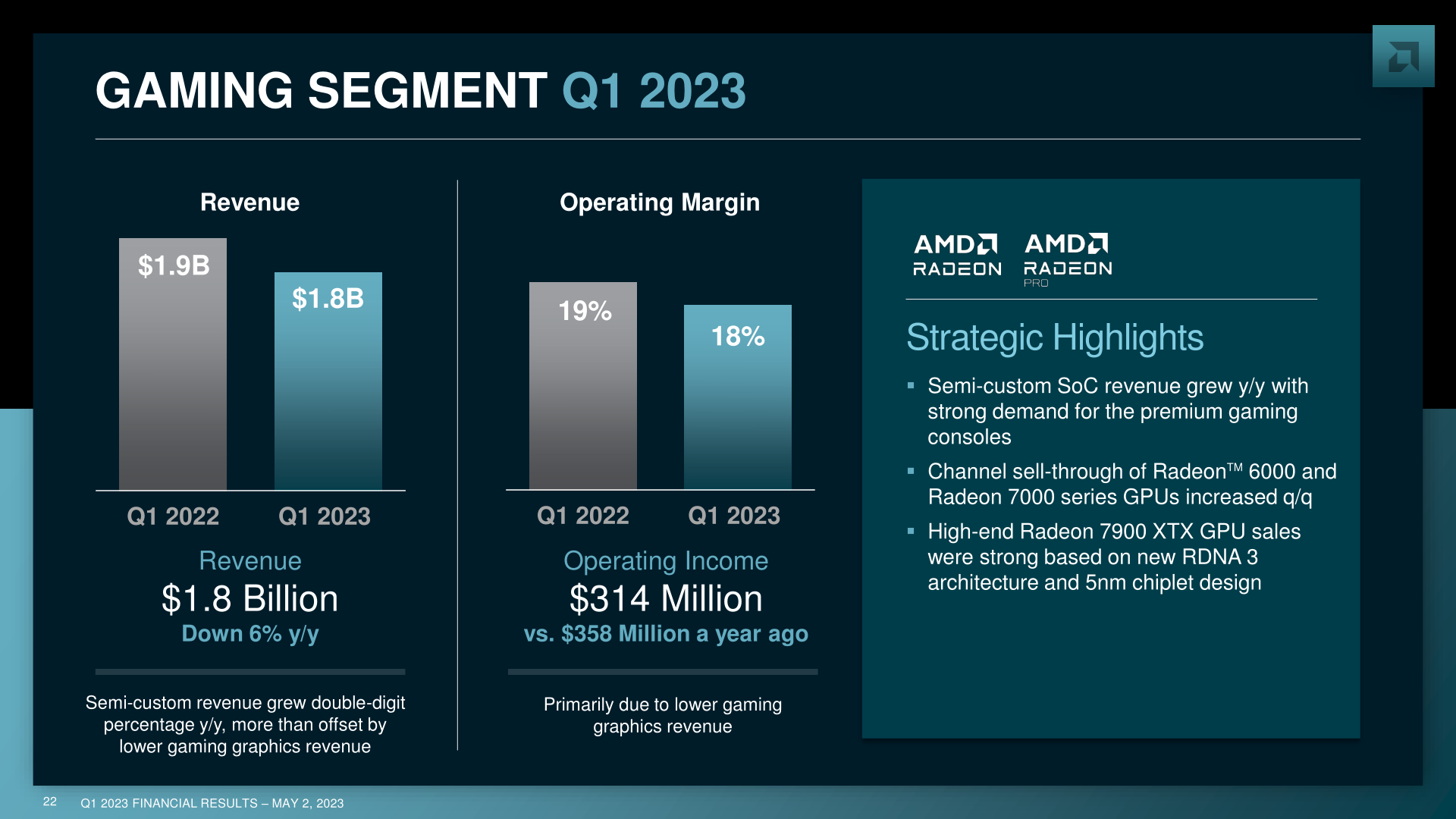

Moving on, AMD’s Gaming segment turned out to be one of the company’s stronger segments for the quarter. The client GPU and semi-custom SoC group did see a year-over-year drop in revenue, but, critically, operating margins saw only slight declines.

For the quarter, AMD booked $1.8B in revenue for the Gaming segment, down 6% from the year-ago quarter. Operating income was $314M, a drop of 12% year-over-year. Of the limited break-out information AMD provides, the company has indicated that client GPU revenue is down by a decent degree, even though total unit sales are up. Preventing a more significant decline in the business has been “double digit” growth in the semi-custom side of the business, with SoC sales for game consoles and other bespoke devices partially offsetting the decline in GPU revenue. This is also why AMD’s operating income for the segment was down some, as those semi-custom products fetch lower margins.

But the real winner among all of AMD’s reporting segments was the Embedded segment, which covers the bulk of Xilinx’s portfolio of FPGAs and other processors, as well as Ryzen and Radeon embedded SKUs. Thanks to the Xilinx acquisition, this segment has seen massive year-over-year growth for the past few quarters, and this is the final quarter where AMD will see those acquisition gains.

For Q1’23, the Embedded segment booked $1.6B in revenue and $798M in operating income, which is an increase of 163% and 188% respectively. Despite the downturn in tech spending, ex-Xilinx products have proven to be relatively better insulated with regards to sales consistency. But more significant still is that embedded products are fetching very high margins – the segment’s operating margin was 51%, far better than any of AMD’s other segments. This kind of consistency and market opportunity is a big part of why AMD wanted to acquire Xilinx in the first place, and that bet is paying off by keeping AMD a bit steadier during this larger tech spending downturn.

The full absorption of Xilinx and the subsequent drop in client sales has made for an interesting and relatively dramatic shift in AMD’s overall revenue split. A year ago, Client was AMD’s leading business segment, and now it’s dead last. Even AMD’s Data Center segment is taking a back seat to both Gaming and Embedded. As former AnandTech editor Dr. Ian Cutress has put it, AMD has quickly become a “client-last” company. This will likely shift some later in the year as the Client market recovers and the Embedded market declines a bit, but AMD may never be a client-first company again – and so far they seem perfectly fine with that.

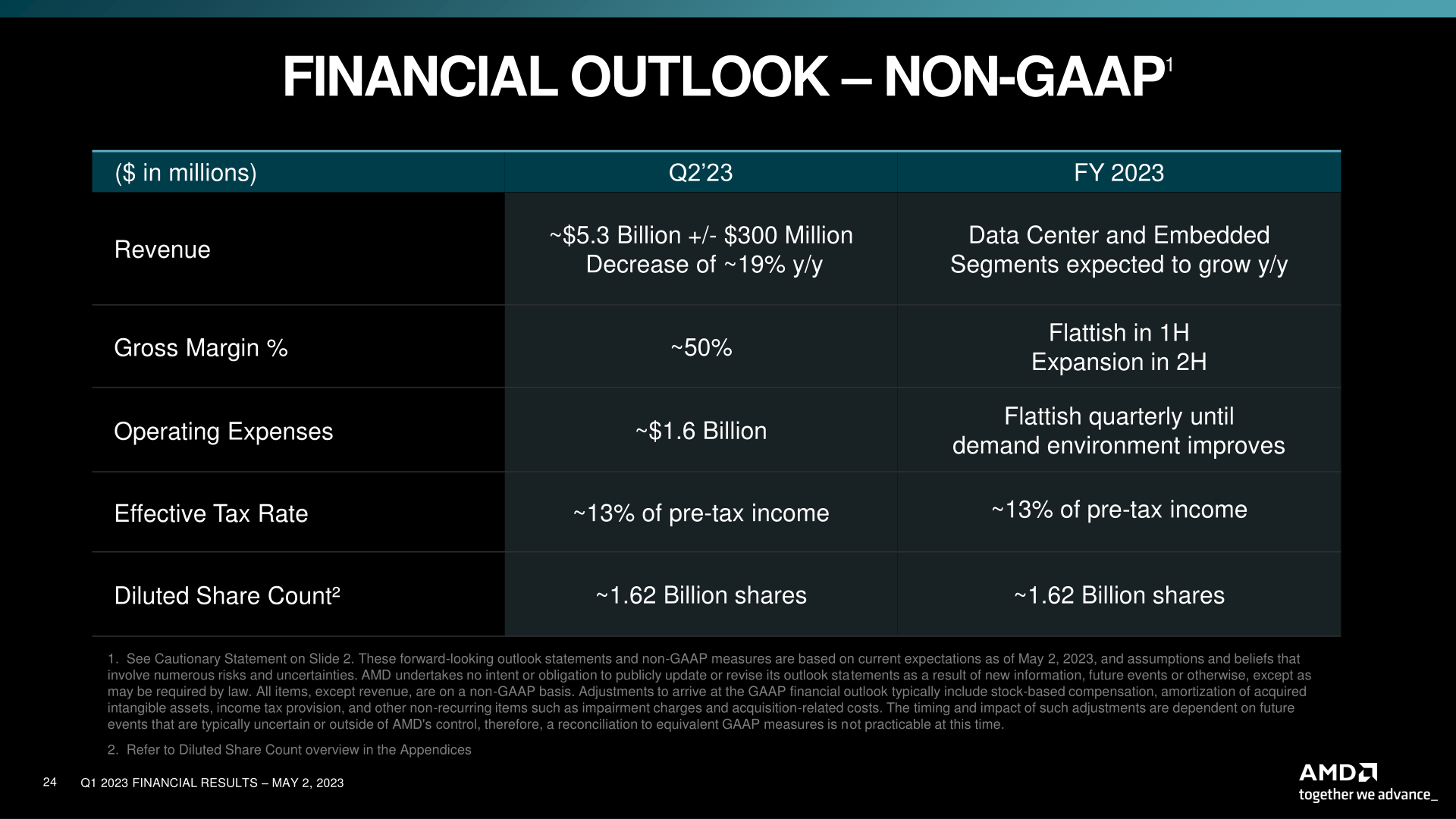

Looking forward, AMD’s recovery plans look a lot like the rest of the industry’s. If Q1 is the bottom, then things will be marginally better in Q2. To that end, AMD is currently projecting $5.3B (+/- $300M) in revenue for Q2, which would be a 19% year-over-year decline. The real recovery in the client and data center spaces is not expected until the second half of the year, when AMD hopes to resume modest growth in those segments.

In the interim, AMD is already preparing for that turnaround. In their earnings report, AMD noted that product inventories have grown slightly on a quarterly basis, to $4.2B. This is being done in anticipation of the ramp of new data center and client products on cutting-edge process nodes. And while it’s not a great look at a time when customers themselves are drawing down their chip inventories, it reflects the long ramp-up times for new products.

Finally, outside of direct financial matters, the most recent earnings cycle has also seen push their AI product narrative a bit harder. Driven in part by antsy shareholders – who have been eyeing the high margins and growth opportunities over at NVIDIA and other AI-adjacent rivals – AMD has been putting extra effort in promoting their AI efforts and current product stack. In some respects, this is an effort to calm investors until Instinct MI300 ships late this year – which should be AMD’s best chance yet to break into the high-end AI training/inference market – but it also reflects an increase in interest from the company. As noted during AMD’s conference call, Victor Peng, Xilinx’s former CEO, has recently been placed in charge of all of AMD’s AI efforts. So while AMD isn’t announcing any new AI roadmaps, it’s clear that they are banking on Xilinx and Peng’s expertise in the area to improve their position in the long run.

Source: AMD